Freedom of Money Transfers

Control when you receive, move, and withdraw your money – not the bank

For decades, money movement has been dictated by banks. Payments could be instant for the customer, but businesses and individuals were forced to wait: next business day, end of the week, or after a bank batch run. In a global, always-on economy, that model is no longer acceptable.

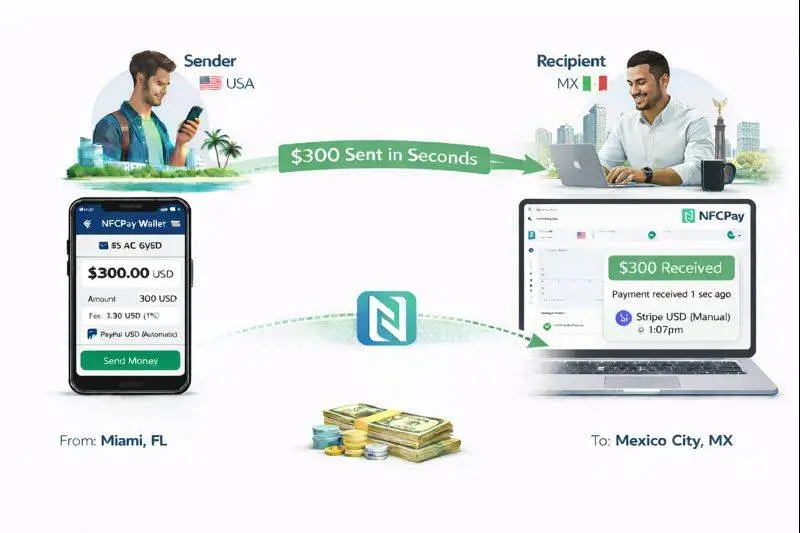

Freedom of money transfers is about changing who controls the timing, flow, and use of funds. With modern digital wallets and payout platforms, payments are no longer locked to bank schedules. Instead, users decide when money moves, how it is paid out, and under which currency conditions.

This is where solutions like NFCPay Wallet, combined with Stripe, represent a fundamental shift in how money works.

From bank-controlled payouts to user-controlled transfers

Traditional Tap to Pay and card-based payment systems usually follow the same pattern:

Payment is accepted

Funds pass through acquirers and banks

Payouts happen on fixed schedules

Currency conversion is often automatic and unavoidable

This works, but it leaves users with very little control. Whether you are a freelancer, a global platform, or a multinational enterprise, you are still waiting on someone else’s clock.

With NFCPay, the logic changes.

Payments are received into a wallet-driven flow, while payouts are managed through the user’s own Stripe account. That means:

Funds are recognized immediately

The user chooses payout timing

Payouts can be automatic or manual

Capital is no longer forced to move on the bank’s schedule

This is not about removing banks — it’s about moving decision-making to the user.

Tap to Pay is only the entry point

Tap to Pay is often misunderstood as the entire solution. In reality, it’s just the front door.

In the NFCPay model, Tap to Pay (and other payment methods) act as:

A fast way to accept payments

A frictionless user experience

A modern alternative to traditional terminals

But the real value starts after the payment is accepted:

Where does the money go?

When can it be withdrawn?

In which currency?

Under what market conditions?

NFCPay focuses on the full money lifecycle, not just the tap.

Stripe payouts: automatic or manual – your choice

Every NFCPay user connects their own Stripe account. This gives direct access to Stripe’s payout controls, without forcing a one-size-fits-all model.

Users can choose between:

Automatic payouts

Funds are transferred on a recurring schedule

Ideal for predictable cash flow

Minimal manual handling

Manual payouts

The user decides exactly when funds are withdrawn

Full control over liquidity

Strategic timing for larger balances

This flexibility is critical — especially as transaction volumes grow.

Why large enterprises benefit the most

While small businesses benefit from faster access to funds, large companies benefit exponentially more.

At enterprise scale, payments are not just transactions — they are capital flows. Delaying or accelerating a payout by even a short time can:

Improve liquidity ratios

Reduce short-term borrowing needs

Increase interest or yield opportunities

Protect margins during volatile periods

Banks typically don’t offer this level of control by default. Wallet- and platform-based models do.

Currency timing: where real money is made

For global businesses, currency is not a detail — it’s a profit lever.

Imagine a company receiving large volumes in USD, EUR, or GBP:

Automatic conversion locks in whatever rate exists that day

Fixed payouts remove strategic flexibility

Margins are exposed to short-term volatility

With user-controlled payouts through Stripe:

Funds can be held temporarily

Exchange rates can be monitored

Conversion can happen when the currency is favorable

When transaction volumes are high, small percentage differences can translate into significant gains — sometimes more than the operational profit itself.

This is why treasury and finance teams increasingly look for timing control, not just payment acceptance.

A global trend backed by data

Global payment statistics consistently show:

Digital wallets growing faster than traditional card-only flows

Real-time and near-real-time payments becoming the norm

Businesses demanding control over payout timing

Platforms replacing banks as the user experience layer

The expectation is clear:

If the payment is completed, access to funds should not be delayed by legacy systems.

NFCPay is built for this expectation.

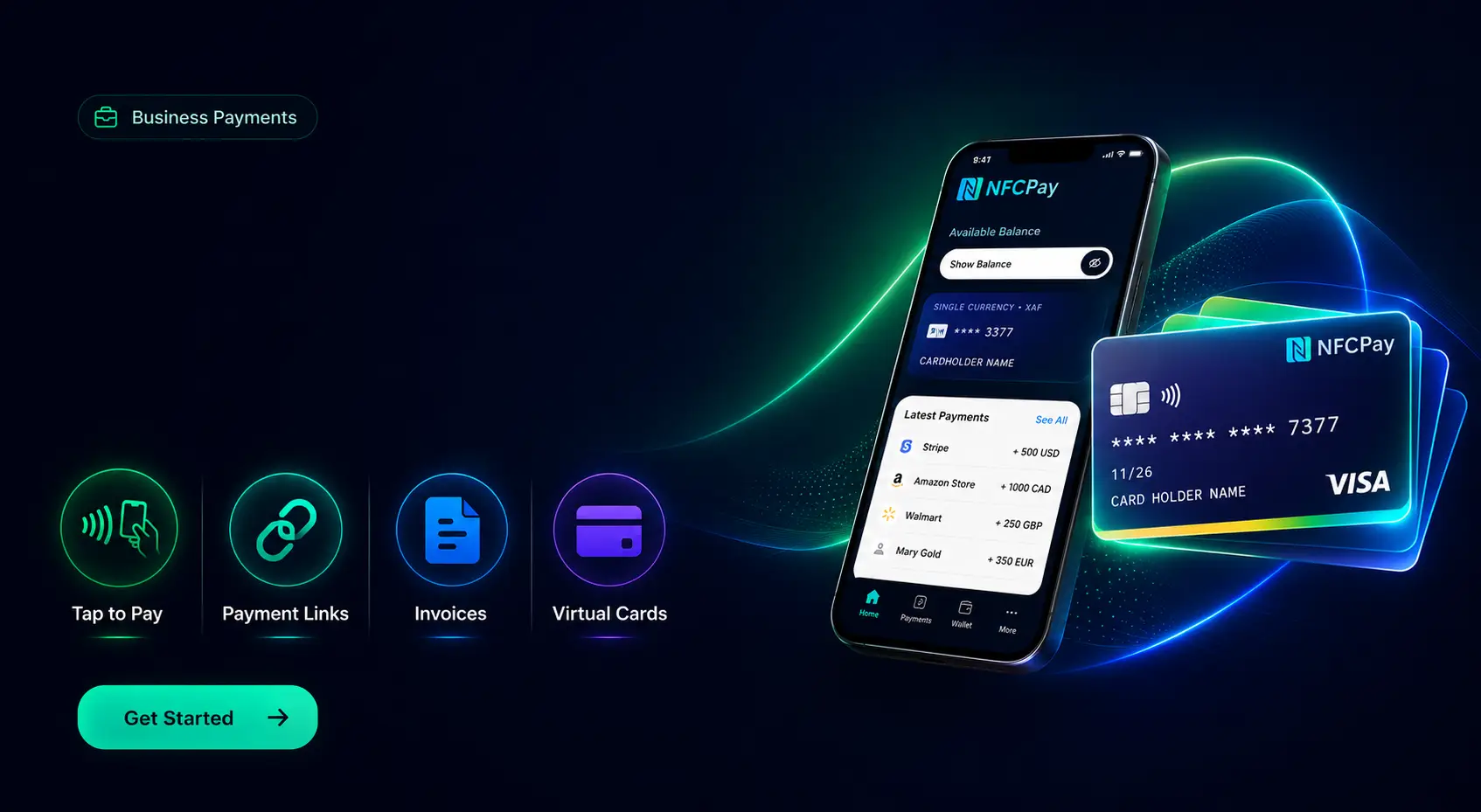

Web and Android: one flow, full control

NFCPay Wallet is designed to work seamlessly across platforms:

Web for administration, monitoring, and payout decisions

Android app for on-the-go payments, transfers, and visibility

No matter the device, users retain:

Visibility over incoming funds

Control over Stripe payouts

Flexibility across currencies and timing

👉 Learn more: https://nfc-pay.com

👉 Download the Android app:

https://play.google.com/store/apps/details?id=net.appdevs.nfcpay&pcampaignid=web_share

Freedom at every scale

For individuals, freedom means:

Getting paid without waiting

Using money immediately

Avoiding bank delays

For businesses, freedom means:

Managing liquidity

Choosing payout timing

Optimizing currency conversion

Turning payment flow into a strategic asset

The larger the amounts, the more valuable this freedom becomes.

Conclusion

Freedom of Money Transfers is not about speed alone.

It’s about control, timing, and choice.

By combining NFCPay Wallet with Stripe’s payout infrastructure, users — from individuals to global enterprises — gain:

Control over when money moves

Flexibility between automatic and manual payouts

The ability to benefit from favorable currency conditions

Independence from rigid bank schedules

In a global, digital economy, money should move on your terms.

And that is exactly what freedom of money transfers means.